You finally find a treatment program that feels right. The staff sounds kind. The schedule works. Your loved one is willing to talk about detox, outpatient care, or medication-assisted treatment. Then the next question lands hard: “Can you verify your insurance?” That's the moment many families freeze. The card in your wallet suddenly feels like …

You finally find a treatment program that feels right. The staff sounds kind. The schedule works. Your loved one is willing to talk about detox, outpatient care, or medication-assisted treatment. Then the next question lands hard: “Can you verify your insurance?”

That's the moment many families freeze. The card in your wallet suddenly feels like it's written in another language. You're trying to make a healthcare decision under pressure, and now you're expected to sort out deductibles, network rules, prior authorization, and whether a telehealth or detox service is covered at all.

The good news is that this process is manageable. It helps to treat insurance verification as a short series of concrete tasks instead of one giant, intimidating problem. That matters because coverage can shift more often than people expect. The healthcare industry changed its approach after recognizing that about one in six Medicare and Medicaid patients experience a change in coverage every month, which is one reason benefit checks need to happen right before treatment begins.

Table of Contents

- The First Hurdle Finding a Path Through the Insurance Maze

- Your Pre-Verification Checklist What to Gather Before You Call

- Confirming Your Benefits Online Portal vs Phone Call

- The Crucial Step of Preauthorization for Treatment

- Navigating Out-of-Network and TRICARE Coverage

- Let Us Help The Easiest Way to Verify Your Coverage

The First Hurdle Finding a Path Through the Insurance Maze

Most families don't start by asking, “What's the group number?” They start by asking, “Can my son get into detox today?” or “Will this program work for my wife?” Insurance enters the conversation because treatment has to be realistic, not because anyone wants to become an expert in billing.

That's why this part feels so frustrating. You may already be carrying fear, urgency, guilt, exhaustion, or all four. Then an insurer asks for exact details about the subscriber, the effective date, the level of care, and whether the facility is in network. It can feel like one wrong answer will stop treatment before it starts.

Coverage verification is not a test. It's a safety check that helps you avoid preventable denials and surprise bills.

For substance use treatment, timing matters. Benefits may look straightforward on the card but work very differently once you ask about detox, medication-assisted treatment, residential care, intensive outpatient services, or telehealth delivered across state lines. A general medical benefit doesn't automatically answer those questions.

A practical way to think about it is this: you're not trying to master insurance in one sitting. You're trying to confirm a short list of facts before care begins. That's also why many families lean on tools and workflows built for medical eligibility verification when they need a clearer process. The point isn't to make insurance feel technical. The point is to make it less chaotic.

What makes addiction treatment verification different

Substance use treatment often triggers extra review because the insurer may separate benefits by level of care. Detox can have one set of rules. IOP can have another. Medication coverage can be handled through a separate pharmacy benefit. Telehealth may follow its own rules too.

That doesn't mean coverage isn't available. It means you want the right answers before admission, not after a claim has already been submitted.

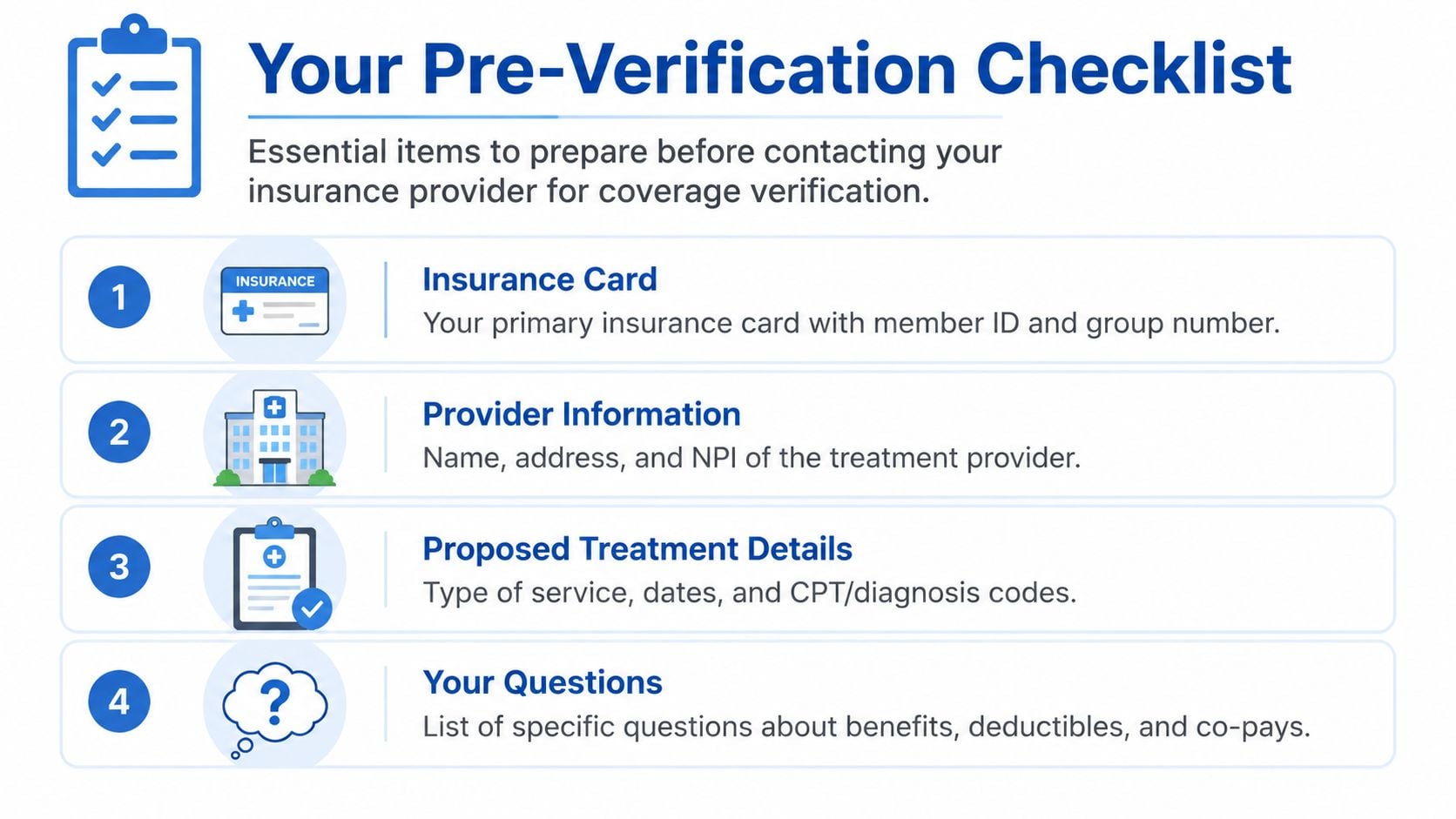

Your Pre-Verification Checklist What to Gather Before You Call

Before you log into a portal or call the number on the back of the card, get your information in one place. That single step saves time, keeps the call focused, and lowers the odds of giving incomplete information.

Claim denials tied to incorrect or missing insurance information cost the U.S. healthcare system over $262 billion annually, and getting the group ID and effective dates right from the start is a key safeguard.

Start with the card and the subscriber details

Have the front and back of the insurance card ready. Insurers and treatment centers usually need more than the member ID alone.

Gather these items before you call:

- Patient basics: Full legal name, date of birth, address, and phone number.

- Insurance identifiers: Policy number, member ID, group number, and plan name exactly as shown on the card.

- Subscriber information: If the patient is covered under a spouse, parent, or partner, have that person's full name, date of birth, and address ready.

- Effective dates: If you've recently changed jobs, switched plans, or renewed coverage, confirm the plan's start date.

- Payer contact details: The member services phone number and any behavioral health phone number listed on the card.

A common mistake is assuming the patient and the subscriber are the same person. In addiction treatment, that can slow everything down, especially if the insurer needs to confirm the patient's relationship to the primary insured before authorizing care.

Know the treatment details before you ask about coverage

The insurer can't give a useful answer if the request is too vague. “Do you cover rehab?” usually leads to a vague answer back.

Bring specific provider and treatment details:

- Provider name and location: The exact facility or program you're considering.

- Level of care: Detox, residential rehab, partial hospitalization, intensive outpatient, medication-assisted treatment, or counseling.

- Timing: Proposed admission date or the date of the first appointment.

- Service format: In person or telehealth.

- Clinical context: A brief summary of why treatment is being sought, if the insurer asks whether the service is medically necessary.

Practical rule: The more precise your questions are, the more precise the insurer's answers will be.

Learn the few insurance terms that matter most

You don't need a billing degree. You only need a working definition of the terms that affect what you'll owe.

| Term | What it means in plain language |

|---|---|

| Deductible | What you pay before the plan starts sharing more of the cost |

| Copay | A fixed amount you pay for a visit or service |

| Coinsurance | Your share of the allowed cost after deductible rules apply |

| Out-of-pocket maximum | The most you should have to pay in covered costs during the plan period |

| Preauthorization | Approval the insurer may require before certain treatment starts |

Write down your questions before you call. That sounds simple, but it keeps families from hanging up and realizing they forgot to ask the one thing that mattered most.

Confirming Your Benefits Online Portal vs Phone Call

Both methods work. They just solve different problems.

For basic benefit checks, the online portal is usually faster. For addiction treatment questions that involve level of care, medical necessity, facility status, or telehealth nuance, a phone call often gives clearer answers.

Success rates for verifying coverage through online provider portals are 96.5%, with 99% accuracy in capturing real-time deductible balances, which is why portals are often the quickest way to confirm straightforward benefit details.

What the portal is good for

Start online if you want to verify the basics without waiting on hold. Most insurers let members review a snapshot of coverage through the website or app.

Use the portal to check:

- Active coverage: Make sure the plan is current and hasn't changed.

- Deductible status: See how much has been met.

- Out-of-pocket maximums: Helpful for understanding worst-case financial exposure under covered care.

- Network lookup: Search by provider or facility name.

- Claims history: Useful if treatment was billed before and you want to see how the plan processed it.

The portal works best when you're checking objective items. It's less reliable when you need interpretation. For example, a portal may show behavioral health coverage but not explain whether medically supervised detox requires prior review, whether an out-of-network exception is possible, or how telehealth addiction treatment is handled.

When a phone call works better

Call the insurer when the treatment is specialized, urgent, or likely to trigger extra rules. Addiction treatment often checks all three boxes.

During the call, ask the representative to answer your questions for the specific level of care you're considering. Don't settle for broad phrases like “behavioral health is covered.” Coverage for weekly therapy is not the same as coverage for detox or IOP.

Here's what to document while you're on the call:

- Representative name: Write it down.

- Date and time: Keep a clean record.

- Reference number: Ask if the call can be tagged with one.

- Exact wording: Especially for network status, authorization rules, and patient responsibility.

- Next step: Whether the provider must submit records, whether the patient must call back, or whether another department handles substance use treatment.

If the answer sounds unclear, ask the representative to repeat it in plain language and confirm what happens before treatment begins.

A script you can use

You don't need to sound polished. You need to be organized.

Try this:

- “I'm calling to verify substance use treatment benefits for a specific provider.”

- “Can you confirm whether the policy is active and the effective date is current?”

- “Is this provider in network for addiction treatment services?”

- “What are my benefits for medically supervised detox?”

- “What are my benefits for intensive outpatient treatment?”

- “Do these services require preauthorization or prior review before treatment starts?”

- “Are telehealth addiction services covered, and are there any location or licensing restrictions I should know about?”

- “If the provider is out of network, what are the out-of-network benefits, deductible, and reimbursement rules?”

- “Can you note this call and give me a reference number?”

If the insurer splits behavioral health from medical services, ask to be transferred instead of ending the call. Substance use treatment benefits are often handled by a dedicated department.

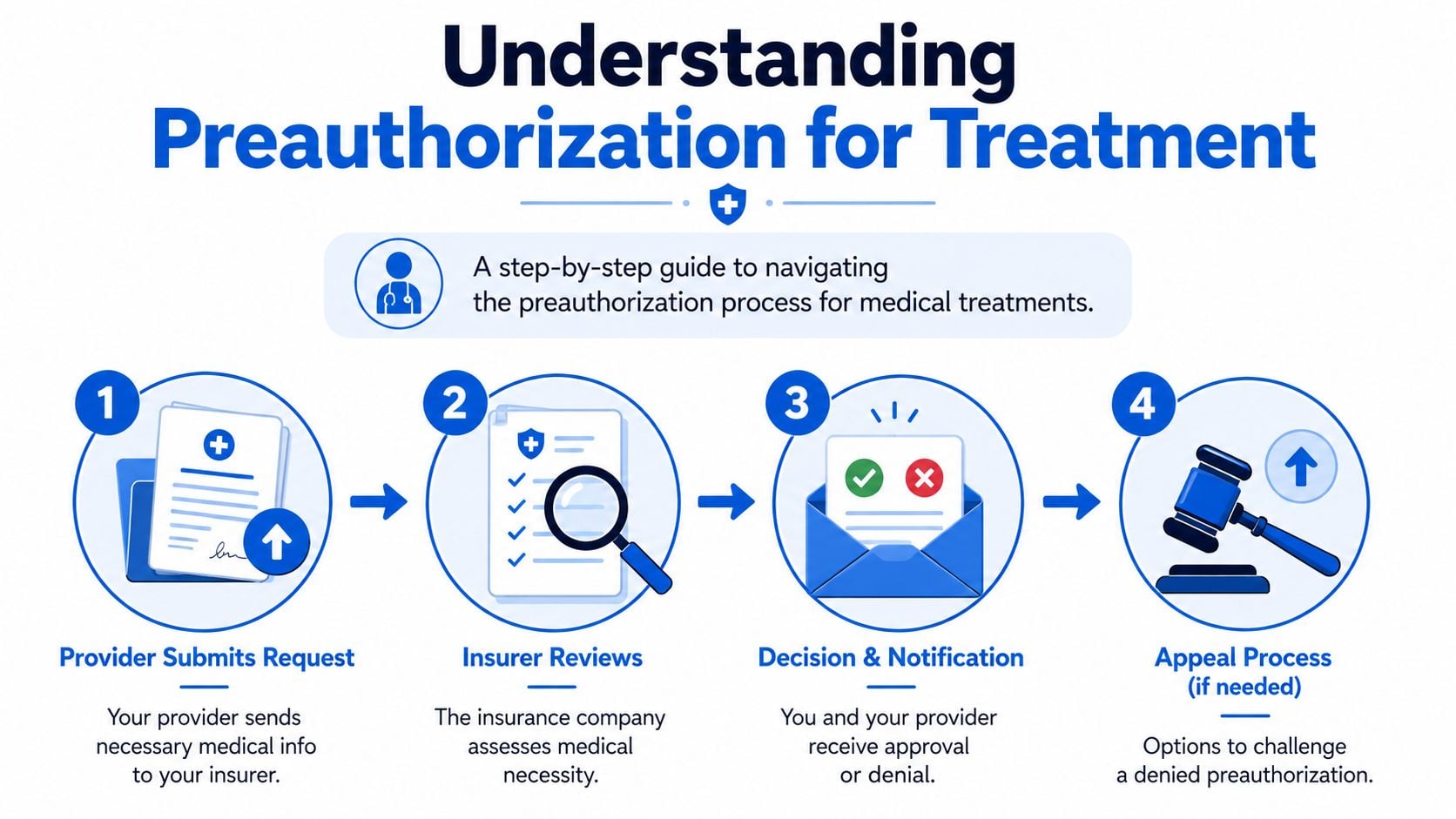

The Crucial Step of Preauthorization for Treatment

Preauthorization is where many families get tripped up because the word sounds more intimidating than it is. In plain terms, it means the insurer wants to review the request before certain treatment begins.

For addiction care, this often comes up with detox, residential treatment, higher-acuity outpatient programs, and some medication-related services. If the insurer requires preauthorization and it isn't completed correctly, the family may hear “you have coverage” and still end up facing a denied claim later.

What preauthorization actually means

This step is about medical necessity. The insurer wants clinical information showing why this level of care is appropriate right now.

For substance use disorders, missing preauthorization paperwork drives a meaningful share of denials. About 22% of denied claims for substance use disorders stem from missing pre-authorization documentation, and automated verification workflows can reduce denials compared with manual phone-only processes.

The key takeaway is simple: a verbal “yes, we cover treatment” is not enough if the plan requires prior review.

What your treatment center usually submits

The provider usually handles the actual submission. That often includes admission details, presenting symptoms, recent substance use history, safety concerns, treatment recommendations, and clinical notes that support the requested level of care.

This video gives a helpful overview of how preauthorization works in practice:

The family's role is usually to provide accurate insurance information quickly and respond if the admissions or clinical team needs clarification. Delays often happen because the card is outdated, the subscriber details don't match, or the plan changed and no one realized it.

What you should confirm before admission

Ask these questions directly:

- Has preauthorization been requested: Don't assume it's automatic.

- For which level of care: Detox and IOP may be reviewed separately.

- Was a decision received: Approval, pending review, or denial.

- What dates were approved: Authorization can apply to a limited period or service window.

- If denied, what happens next: Clarification, peer-to-peer review, or appeal.

“Covered” and “authorized” are not the same thing. For higher levels of care, you usually want both confirmed.

Families often feel awkward asking these questions because they don't want to slow the process. In reality, asking them early is what keeps the process moving.

Navigating Out-of-Network and TRICARE Coverage

A family may do everything right, find a detox or IOP program with an opening, and then hit a new problem. The facility is out of network, or the insurance card says TRICARE and no one is sure what that changes. That moment is common in substance use treatment, especially when the safest or fastest option is not the closest contracted provider.

Out-of-network does not always mean no coverage

Out-of-network coverage can still exist. The harder part is figuring out how much the plan will pay, what paperwork is required, and whether the family can manage the remaining balance.

For substance use treatment, those details matter more than they do in many routine medical visits. Detox, medication-assisted treatment, and telehealth IOP are often limited by geography, bed availability, or clinical fit. A family may not be choosing an out-of-network option for convenience. They may be choosing the first safe option that can admit their loved one.

A short outside reference like Benely's guide to network health plans can help clarify the language plans use before you call.

Here is the practical difference:

| Scenario | What usually happens |

|---|---|

| In-network care | The provider has a contract with the plan, and member cost-sharing is usually more predictable |

| Out-of-network care | The plan may pay a portion of the cost, but the patient often owes more and may need to submit or support extra documentation |

The two out-of-network numbers families often miss are the separate deductible and the reimbursement basis. Some plans reimburse based on a percentage of their allowed amount, not the provider's actual billed rate. That gap can leave a much larger balance than the family expected.

Questions to ask about out-of-network addiction treatment

Ask for clear answers to these points:

- Does the plan include out-of-network substance use treatment benefits

- Is there a separate out-of-network deductible

- What is the reimbursement method for this level of care

- Does the plan require preauthorization for out-of-network treatment

- Is a single-case agreement or gap exception possible if no appropriate in-network provider is available

- Are telehealth addiction services treated differently when the provider is outside the local area

If the representative says out-of-network care is covered, keep going. Ask under what conditions, at what reimbursement rate, and what the patient is likely to owe for detox, residential care, or IOP specifically.

That follow-up matters. I have seen families hear “yes, it's covered” and assume the hard part is over, only to learn later that the plan applied a high deductible, limited the allowed amount, or required a separate review because the provider was outside the network.

How TRICARE fits into substance use treatment

TRICARE can cover substance use treatment, but verification usually takes a little more care. The answer may depend on the sponsor status, plan type, referral rules, region, and the level of care being requested. Detox and outpatient services do not always follow the same path.

Military families should verify:

- Plan type and beneficiary status

- Whether a referral is required

- Whether preauthorization applies to the requested level of care

- Whether telehealth services follow any additional rules

- What the patient's share of cost may be

With TRICARE, I tell families to slow down and confirm the sequence, not just the benefit. A service can be part of the plan and still run into delays if the referral path, authorization requirement, or provider status is not lined up correctly before admission.

That is especially important for substance use care, where timing matters. If someone needs detox now, or an urgent step down into IOP, the fastest way to avoid an insurance surprise is to verify the level of care, the authorization rules, and the network status together.

Let Us Help The Easiest Way to Verify Your Coverage

By the time families finish this process on their own, most of them say the same thing: “I could do it, but I don't want to do it again.” That reaction makes sense. Insurance verification is detailed work, and substance use treatment adds another layer because level of care, preauthorization, and network status all have to line up.

Many industries solve that kind of administrative burden by handing the task to teams that do it every day. The same logic sits behind models like insurance process outsourcing. In treatment admissions, the goal isn't corporate efficiency. It's giving families a clear answer quickly, while they focus on getting someone help.

Why many families hand this off

A strong verification process doesn't just ask whether the policy is active. It checks whether the treatment being considered matches the benefit structure, whether prior review is needed, whether the subscriber details match, and whether the expected patient responsibility is understood before admission.

That's hard to do when you're also trying to support a loved one in crisis.

Handing off verification is often the easiest path because the admissions team can:

- Collect the right identifiers early

- Contact the payer with the correct treatment details

- Confirm whether authorization is needed

- Clarify likely financial responsibility in plain language

- Flag follow-up items before the first appointment or admission

What to expect when someone verifies benefits for you

A good intake process should feel calm, not rushed. You provide the insurance card and a few identifying details. The team checks benefits, follows up on missing information, and tells you what is confirmed, what is still pending, and what questions remain.

You should also expect honesty. Sometimes the answer is straightforward. Sometimes coverage exists but requires authorization. Sometimes out-of-network rules make the financial picture more complicated. Clear guidance matters more than a fast but incomplete answer.

If you'd rather not spend your day on hold with an insurer, call or text 530-625-7910 any time, day or night, and ask for help verifying coverage. If phone calls feel hard right now, you can also start through the insurance verification form on Addiction Resource Center's website.

If you're trying to figure out treatment costs, coverage, or the next step for yourself or someone you love, Addiction Resource Center LLC can help you verify insurance and understand your options before care begins. Reach out by phone or text at 530-625-7910 for a confidential conversation.