An intensive outpatient program costs somewhere between $3,000 and $10,000 for a full course of care. But the number that matters most isn't the sticker price. It's what you will owe after insurance, because the wrong network choice can turn a manageable bill into something far more serious. If you're reading this right now, you …

An intensive outpatient program costs somewhere between $3,000 and $10,000 for a full course of care. But the number that matters most isn't the sticker price. It's what you will owe after insurance, because the wrong network choice can turn a manageable bill into something far more serious.

If you're reading this right now, you may already have a loved one asking for help, or you may be the one trying to figure out treatment before things get worse. In that moment, the pricing can feel confusing fast. One program quotes a full package. Another talks in daily rates. An insurance card says "behavioral health covered," but nobody explains what that means for your real out-of-pocket cost.

That confusion is common. Families often assume the biggest question is, "How much does IOP cost?" In practice, the bigger question is, "What will insurance cover, and what financial traps should I avoid before enrolling?"

This guide walks through that step by step, in plain language, so you can compare programs calmly, ask better questions, and avoid the out-of-network mistakes that create the worst surprises.

Table of Contents

- Demystifying Intensive Outpatient Program Costs

- What Drives Your Final IOP Cost

- Using Insurance to Make IOP Affordable

- In-Person vs Telehealth IOP Pricing

- Questions to Ask Before Enrolling in an IOP

- Getting Clear Answers in Yuba City

Demystifying Intensive Outpatient Program Costs

A family calls in after seeing two IOP quotes on the same afternoon. One sounds manageable. The other is several times higher for what seems like the same kind of care. That kind of price gap is frightening, and it often happens because the quotes are not built the same way.

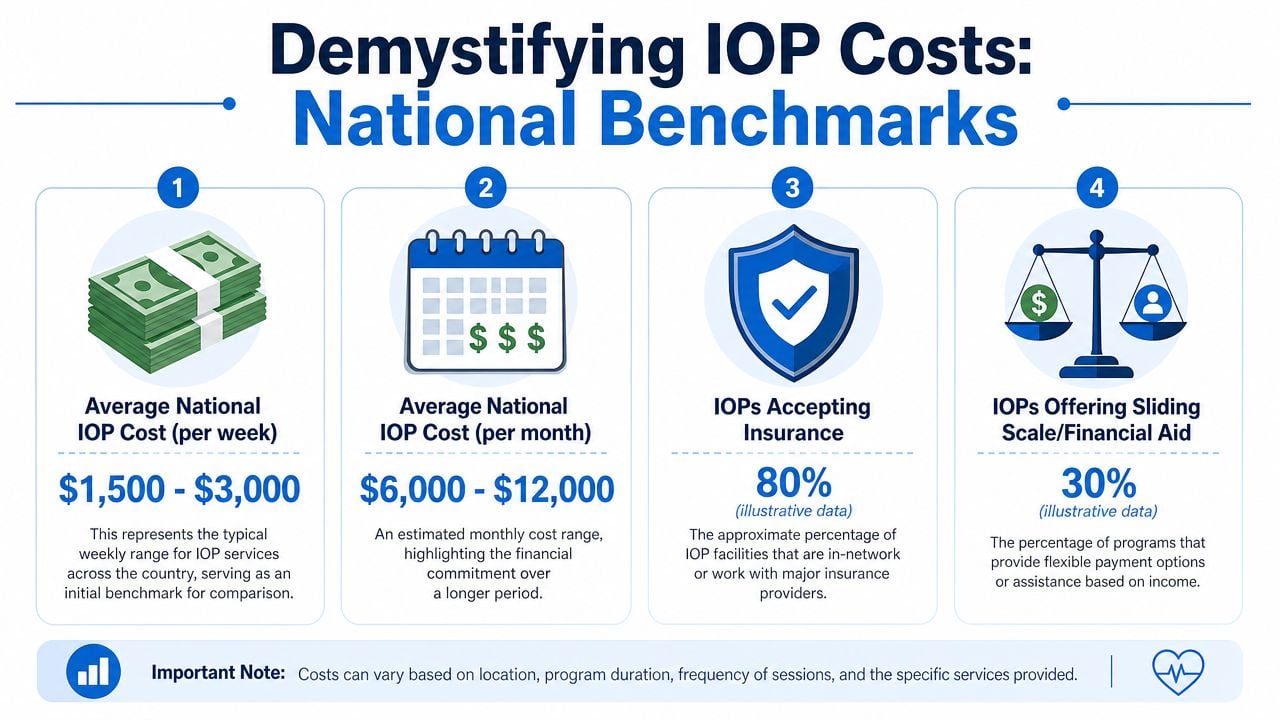

A common benchmark can help you get oriented first. Many IOPs in the U.S. fall in the $3,000 to $10,000 range for a full course of care, and some private facilities bill $250 to $500 per day, according to this overview of IOP structure, costs, and benefits.

The hard part is that a low-looking quote and a high-looking quote may be measuring different things. One program may list a daily rate. Another may give a price for several weeks of treatment. A third may quote only the portion before insurance processes the claim. Until those pieces are lined up side by side, the numbers can mislead you.

What the price usually refers to

IOP is structured treatment delivered over multiple hours each week. Medicare's coverage model is a helpful frame because it describes IOP as care for people who need at least 9 hours of therapeutic services each week, often including group therapy, individual counseling, education, and medication management.

That means the quoted price usually refers to a bundle of clinical time, staff support, and scheduled services over a defined period. It works a lot like comparing child care plans or college tuition. The weekly schedule, number of sessions, and level of professional support shape the total more than the label alone.

This is also where families can get trapped by out-of-network billing. An out-of-network IOP can leave you with bills that are 3 to 5 times higher than you expected because the program's full rate may be far above what your insurance recognizes, and the unpaid difference can become your responsibility. Many articles stop at "check your insurance." The safer question is, "Is this program in network, and if not, what exact dollar amount could I owe after insurance pays its portion?"

Practical rule: Do not compare one program's daily rate to another program's full-course quote until you know the weekly hours, expected length of care, network status, and whether the estimate is the gross charge or your likely out-of-pocket amount.

What the price covers

Families often hear "outpatient" and assume it means occasional appointments. A true IOP is closer to a part-time treatment schedule. The cost usually reflects several layers of care working together:

- Group therapy: The main part of many IOP schedules, often several times each week.

- Individual sessions: Time with a therapist or counselor to address personal goals, triggers, and setbacks.

- Medication support: Oversight for people who need prescription review or medication management.

- Education and relapse prevention: Practical skill-building for daily life outside treatment hours.

- Care coordination: Scheduling, treatment planning, progress reviews, and communication about next steps.

That is why staying at home does not always mean a low bill. You are paying for clinician time, treatment planning, and repeated therapeutic contact over many weeks.

If insurance costs have felt confusing in general, you are not alone. Some families find it helpful to get broader context by reading about understanding high health insurance premiums before they compare IOP benefits, deductibles, and network rules.

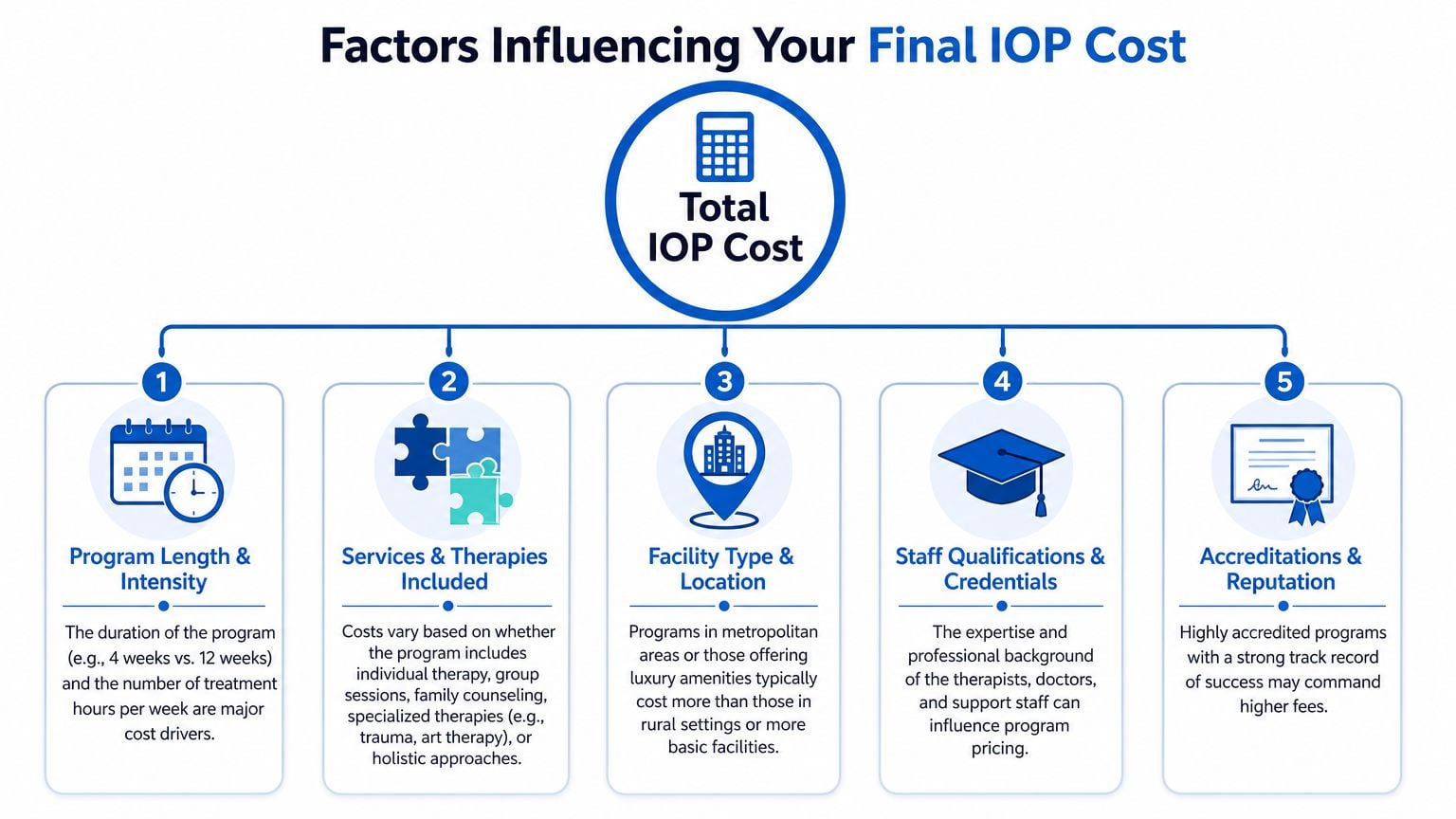

What Drives Your Final IOP Cost

Two intensive outpatient programs can both sound reputable and still have very different price tags. That isn't always a red flag. Often, it reflects differences in the actual treatment product you're buying.

A useful starting point comes from the treatment model itself. A review published in the National Library of Medicine reported that in 2011, there were 6,089 programs in the United States offering IOP services, representing 44% of 13,720 addiction treatment programs nationwide. That same review describes the standard IOP dose as a minimum of 9 hours per week in three 3-hour sessions, with many study samples showing 50% to 70% abstinence at follow-up. You can see those figures in the review of intensive outpatient treatment programs.

Clinical hours shape the price

That historical standard explains a lot. IOP was built to provide substantial care while letting people live at home. If one program offers the baseline level of support and another provides more hours, more family work, or more medication oversight, the second program may cost more because it uses more clinician time.

Think of the bill as having three basic building blocks:

| Cost driver | Why it matters |

|---|---|

| Hours per week | More treatment hours usually mean more staff time and higher overall cost |

| Length of stay | A shorter program and a longer program can have very different totals even if the weekly schedule looks similar |

| Type of services | Programs with more individual therapy, medication oversight, or specialized tracks may price differently |

Why two programs can look similar but cost differently

The treatment setting also matters. A hospital-based outpatient department, a private center, and a community program don't necessarily price care the same way. Neither do regions with different labor costs and overhead.

Staffing can change the quote as well. A program that relies on licensed therapists, medical oversight, and coordinated support may cost more than a lighter-touch model. That's not automatically better or worse for every patient. It means you should ask what level of expertise is included.

The best comparison isn't "Which one is cheapest?" It's "Which one offers the right level of care, and what exactly is included in that price?"

A program's reputation and organization can also influence cost. Some centers offer strong scheduling support, better communication with families, or more detailed discharge planning. Those features may not show up in a headline price, but they can affect value.

When people feel overwhelmed by wildly different quotes, I usually suggest a calmer way to compare them:

- Start with weekly hours. Make sure you're comparing a similar level of intensity.

- Ask how long the program usually runs. A lower weekly cost can still lead to a higher total bill if the program lasts much longer.

- List included services. Medication visits, family sessions, and assessments may or may not be part of the base rate.

- Ask who provides the care. Credentials matter, especially when someone has both substance use and mental health needs.

That approach doesn't eliminate every pricing difference, but it quickly shows whether two programs are comparable.

Using Insurance to Make IOP Affordable

Insurance is where the financial picture becomes either manageable or dangerous. The single biggest factor isn't usually the brochure price. It's whether the program is in-network with your plan.

When people say, "My insurance covers treatment," I always want to slow that sentence down. Covered doesn't always mean affordable. Covered doesn't always mean approved. And covered definitely doesn't mean every treatment center will cost you the same amount.

The in-network decision matters most

One source that lays this out plainly notes that choosing an out-of-network IOP can be financially catastrophic. In-network coverage may pay 60% to 100% of the cost, while out-of-network benefits can fall to 0% to 20%, and patients may end up paying 3 to 5 times more. That same source also warns that this is especially serious for Medicare and TRICARE users, where out-of-network limits can leave families with unexpectedly large bills. Those details appear in this guide to IOP costs and insurance risks.

That's the trap most families don't see coming. They call a center, hear "we accept your insurance," and assume the hard part is over. But "accept" can mean the provider will bill your plan. It doesn't always mean the provider is contracted at your in-network rate.

Ask one direct question: "Are you in-network with my exact plan, not just my insurance company?"

That last part matters. A center may work with Blue Cross generally, for example, but not with your specific employer plan, marketplace plan, or behavioral health carve-out.

The same caution applies to government coverage. Medicare beneficiaries need to confirm that the setting qualifies under current rules. TRICARE families should verify network status before treatment starts, not after the first claim lands.

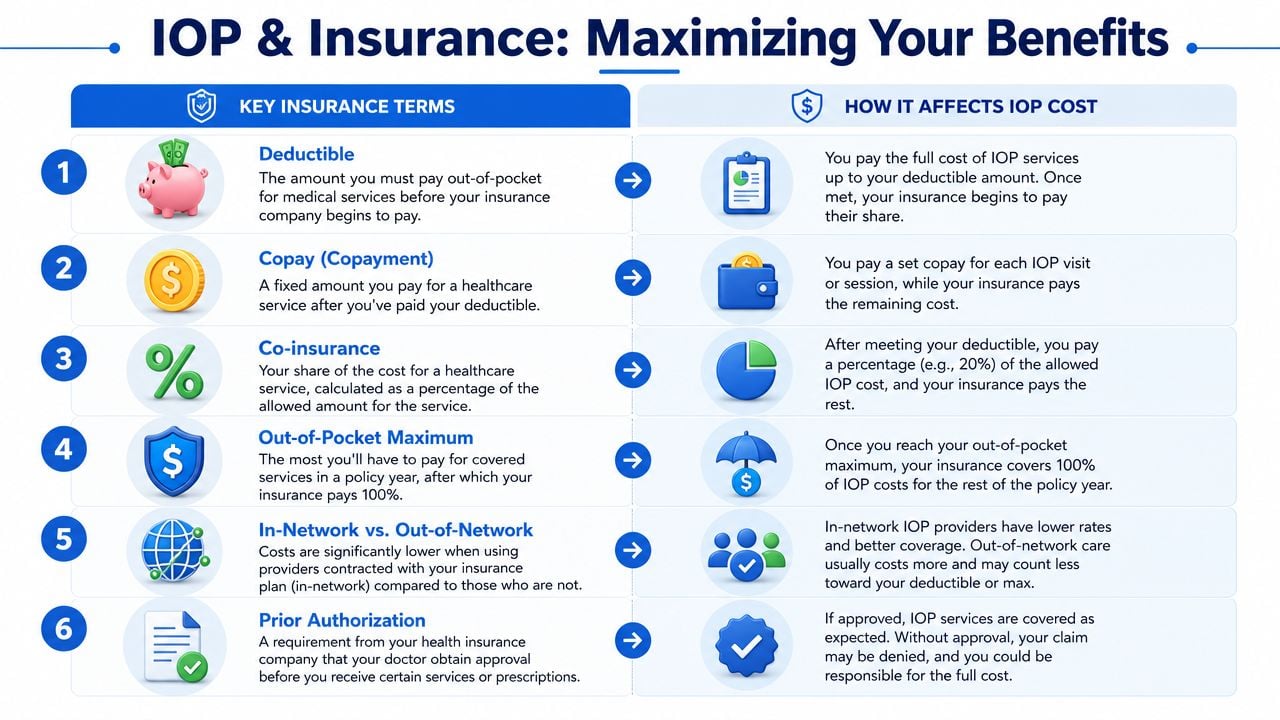

Terms worth understanding before you call

The good news is that you don't need to become an insurance expert. You only need a few terms in plain English.

- Deductible: The amount you may need to pay before insurance starts sharing costs.

- Copay: A fixed amount for a covered service, if your plan uses copays.

- Coinsurance: Your percentage of the allowed amount after the deductible rules are met.

- Out-of-pocket maximum: The most you should pay for covered services during the policy year, according to your plan rules.

- Prior authorization: Approval your insurer may require before treatment begins.

A short visual can help if these terms all blur together at once:

There is another important Medicare detail worth knowing. A policy summary on the 2024 benefit change explains that Medicare Part B now covers medically necessary IOP services at 9 to 19 hours per week in approved in-person settings, but virtual IOPs are not covered under that rule. The summary is available through this explanation of Medicare's IOP coverage change.

That means two programs can seem similar clinically but work very differently financially depending on whether they are in person or virtual, and whether your payer recognizes that setting.

A simple script for your insurance call

You don't need a polished speech. A short checklist works better. Call the number on the back of your insurance card and ask:

- Is intensive outpatient treatment covered under my plan?

- Do I need prior authorization before starting?

- Is this provider in-network with my exact plan?

- What is my deductible, and has any of it been met?

- What will I owe as copay or coinsurance for IOP?

- Does my plan have a separate behavioral health company managing benefits?

- Are telehealth IOP services covered the same way as in-person services?

- Can you give me a reference number for this call?

Write down the representative's name, the date, and the reference number. If a treatment center offers a benefits verification, that's helpful, but I still encourage families to hear the answer directly from their own insurer too.

A good benefits check should answer two separate questions: "Will my plan cover this level of care?" and "Is this exact provider in-network?"

If you only confirm the first question, you're still exposed to the biggest cost surprise.

In-Person vs Telehealth IOP Pricing

A family often calls expecting telehealth to be the budget option. On the surface, that makes sense. There is no drive across town, no waiting room, and fewer facility costs. But IOP pricing works more like hiring a skilled team than renting a room. The largest share of the cost is still the clinical time built into the program.

That is why virtual IOP can land surprisingly close to in-person pricing. Group therapy still needs licensed staff. Individual sessions still take one-on-one clinician time. Medication support and care coordination still have to be covered. The screen changes the setting, but not the work involved in treatment.

American Addiction Centers notes that virtual IOP episodes can still cost several thousand dollars, even though they are delivered online, because staffing remains the main cost driver in care. Their overview of virtual intensive outpatient treatment costs helps explain why online care is not automatically a low-price option.

Why the real price gap often comes from insurance, not format

This is the part many guides skip. The biggest difference is often not telehealth versus in person. It is in-network versus out-of-network.

A telehealth program can look convenient and affordable at first glance, especially if it serves your state from a distance and offers quick admission. But if that provider is out-of-network, the final bill can jump far beyond what a nearby in-person program would cost. Families sometimes end up facing charges that are 3 to 5 times higher than expected because the plan pays only a small share, or nothing at all, once out-of-network billing enters the picture.

That is the expensive trap. The format gets the attention. The network status drives the risk.

How to compare the two without getting burned

A safer question is, "Which option fits my daily life and my exact insurance benefits?"

In-person IOP may make sense if leaving home helps you focus, being physically present improves accountability, or your plan gives clearer coverage for office-based care. Telehealth may make sense if transportation is hard, work hours are tight, or childcare would otherwise delay treatment.

Use this quick filter:

- Choose in-person if structure outside the home helps you stay engaged and your insurance cost estimate is clearer for facility-based care.

- Choose telehealth if attending from home removes real barriers and your insurer confirms the provider is in-network for virtual IOP, not just mental health services in general.

- Slow down before enrolling if a virtual program sounds much cheaper but will not give you a written benefits estimate or a clear answer about network status.

One more point causes confusion. Telehealth can lower side costs, such as gas, parking, time away from work, or arranging a ride. Those savings matter. But they do not cancel out a bad insurance fit. Saving a few hundred dollars in logistics does not help if an out-of-network virtual program leaves you with a bill in the thousands.

So virtual care can be the right fit, but it should not be treated as automatically low-cost.

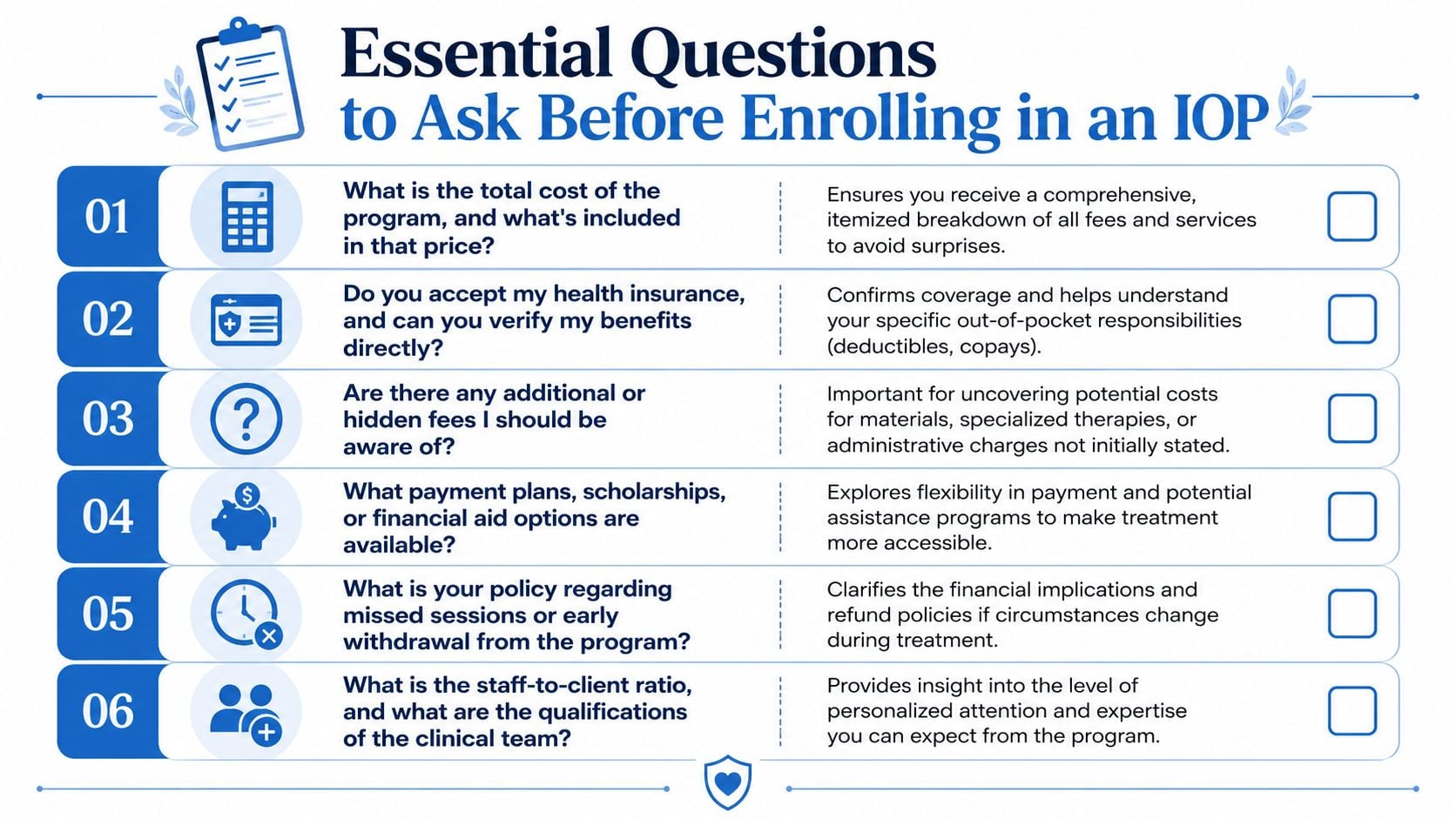

Questions to Ask Before Enrolling in an IOP

When you're calling treatment centers, "How much is it?" is too broad to get a reliable answer. A better conversation asks for the total picture.

Questions for the treatment center

Use these questions almost word for word if you want to avoid vague replies:

- What's the total program cost? Ask whether the quote covers the full course of care or only a daily or weekly rate.

- What's included in that amount? You want to know if individual therapy, group sessions, family work, assessments, and medication visits are part of the price.

- Are there separate charges? Ask specifically about drug testing, intake fees, paperwork fees, missed-session fees, and discharge planning.

- Are you in-network with my exact insurance plan? Not just the insurance brand.

- Will you verify my benefits before I enroll? A solid admissions team should be willing to help.

- Can you give me an estimate of my out-of-pocket responsibility in writing? Estimates aren't guarantees, but written detail is still better than a verbal summary.

If a program won't clearly explain what's included, that's a reason to slow down.

Questions for your insurance company

Then make your own call to the insurer and compare answers.

- Is this provider in-network under my plan?

- Is prior authorization required for IOP?

- What part of the cost am I responsible for?

- Does my plan treat virtual and in-person IOP differently?

- Is there anything that could make a claim deny after treatment starts?

You're listening for consistency. If the center says one thing and the insurer says another, stop and resolve that before the first session.

A simple notebook page works well here. Write the center's answer in one column and your insurer's answer in the next. When those answers match, you can move forward with much more confidence.

Getting Clear Answers in Yuba City

If you're in Yuba City or elsewhere in Northern California, the hardest part may not be finding a program. It may be getting a straight answer without feeling rushed, pressured, or confused.

Clear financial guidance matters because treatment decisions often happen during a crisis. Families are trying to act quickly while also protecting themselves from a bill they didn't expect. That's why it helps to work with a team that can slow the process down just enough to explain benefits, verify insurance, and tell you what the numbers likely mean in real life.

For many people, the best next step is simple. Call a program and ask them to verify your benefits before you commit. Confirm whether care is in-network. Ask whether the estimate includes the whole course of treatment or only part of it. If you need telehealth, ask whether your payer handles that format differently.

A good admissions conversation should leave you feeling steadier, not more confused. You should come away knowing what level of care is being recommended, what insurance information still needs to be confirmed, and what questions remain unanswered.

When those basics are handled well, cost becomes something you can plan around instead of something that controls the decision.

If you want help sorting through these questions locally, Addiction Resource Center LLC in Yuba City can walk you through your options with clarity and compassion. The team works with most major insurance plans, welcomes TRICARE beneficiaries, and offers both in-person and telehealth IOP, along with detox, MAT, and residential coordination through its partner program. You can call or text their 24/7 line at 530-625-7910 to verify benefits, ask about likely out-of-pocket costs, and get straightforward guidance without pressure.